With the recent GST rate cuts, we have observed a significant increase in auto sales. And, Maruti and its investors are happy to see the spike in small car sales. So, today’s topic for discussion is Maruti Suzuki and its resurgence in the small car market. It has been a long time since I shared anything.

Let us look at what has happened, some future expectations, and what the fundamentals of the company look like. Finally, I will share my thoughts on the company and where it is headed.

Positive impact on entry-level car sales

Maruti is well-known for its small and affordable cars. But, for a long time, the sales in that segment remained sluggish. The entry-level cars are mainly sold targeting the middle and lower middle-class population of the country. But due to heavy price inflation and other financial burdens faced by them, they couldn’t afford these cars. Even the company has opined that it is the affordability issue among the people that affects the growth in this segment.

So, the company started focusing more on SUVs and other high-end cars. But with the GST rate cut, which came into effect on 22nd September 2025, they noticed a sudden spike in bookings in low-end cars. It was anticipated spike. But this might not reflect in this quarterly result because the sales weren’t impressive from mid-August till 22nd Sep.

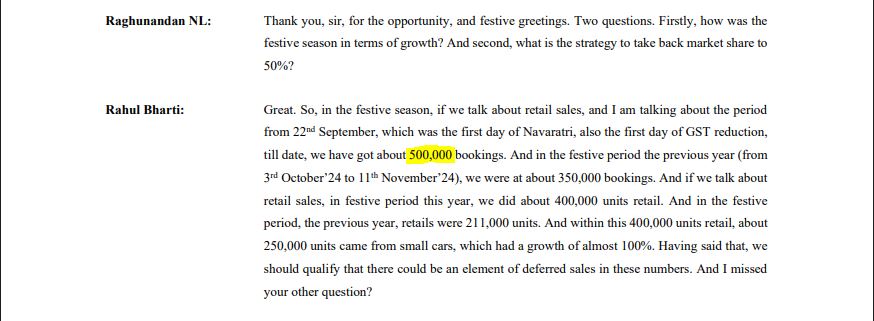

Further, during the earnings call, the company mentioned that with the GST cut, they got about 5,00,000 bookings.

Can this momentum, created by the GST cut, be sustained?

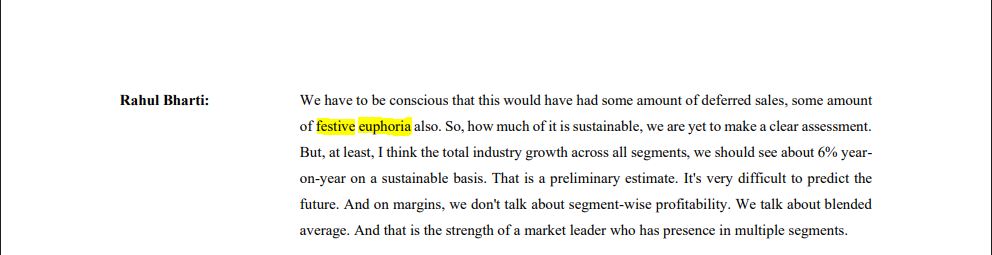

Though we see a strong momentum initially, we should note that it was a festival season. The company says it could be because of the festive euphoria, and only with the changing market trends, the sustainability of this momentum could be ascertained. However, the normal demand [other than festive demand] in this segment too is expected to be higher due to lesser the price.

Position of Maruti in the SUV segment

As mentioned earlier, when their entry-level car segment started underperforming, the company started focusing on SUV segment. With the launch of cars like Victoris, they are trying to strengthen their position in this segment. Further, they have plans to launch eight more SUVs by the FY 2030-31.

How is the fundamentals of this company? A short outlook

The company commands a huge market share of around 40% in the India’s passenger vehicle segment. With strong fundamentals, the company doesn’t seem overvalued currently.

When it comes to production, the company has achieved a milestone of producing 2 million units in the FY 2024-25, based on their Annual Report [PDF file]. Further, they are aiming to achieve an annual capacity of 4 million units by FY 2030-31. To achieve this, the company has added a capacity of 1,00,000 units in the Manesar Facility and a capacity of 2,50,000 units has been commissioned at the Kharkhoda Facility. The production has been initiated at the Kharkoda Facility, you can explore more about the Kharkhoda Facility here.

The company’s product portfolio include hatchbacks, utility vehicles [UVs], light commercial vehicles [LCVs], and vans. The management has commented during the earnings call that, in total Maruti Suzuki has more than 5,000 service touchpoints spaning 2,818 cities across India. These workshops include the workshops of Arena and Nexa, rural workshops, sales and service points, service-on-wheels, and Maruti Suzuki authorised service stations.

Above all the company has seen growth in exports. In the second quarter, Maruti comanded nearly 45.4% share in the India’s total passenger vehicle exports.

Final Takeaway

The company with a good history of showing consistent growth over the years, is expected to grow further. The management is expecting an overall growth of 6% consistently year-on-year. Yet macro economical risks still exist. I mentioned above that from the mid-August till 22nd Sep, the financials weren’t impressive. It was because of various negative factors like forex fluctuations, more advertisement expenses, and increase in the employee cost. Increase in the employee cost and the advertisement expenses can be treated as normal. The company mentioned that, they had to work even on sundays to match the demand. Further they had a new launch, which needed promotion. But, the forex fluctuations are beyond the control of the company.

Excluding those short-term macro economic factors, the company undoubtedly has a good future. Despite the competition from other automible giants, they try to sustain and regain its 50% market share. They are focusing more on innovation. Usually its cars are complained for lower body strength. But one of their cars, recently launched, received a 5-star safety rating in Bharat-NCAP for both adult and child occupation protection.

All these clearly indicate their dedication towards regaining the 50% market share. All these things are just my views. So if you are willing to invest in this company I request you to do your own research, or do consult a SEBI Registered investment advisor before you decide to invest in this company. The future is always uncertain.

With that note, I’m ending it here.